Now that Bernie Sanders is again firing up the discussion about single-payer health insurance, it might be a good idea to review this complex issue. So, here’s a short self-test for you to gauge your understanding of what Bernie, and a lot of other people, are talking about. The correct answers are supplied right away, so you won’t stay confused for long. Since this is an internet-based test, YOUR ANSWERS, of course, WILL BE COMPLETELY ANONYMOUS. Nothing will be recorded by NSA , Equifax, or the Russians.

Now that Bernie Sanders is again firing up the discussion about single-payer health insurance, it might be a good idea to review this complex issue. So, here’s a short self-test for you to gauge your understanding of what Bernie, and a lot of other people, are talking about. The correct answers are supplied right away, so you won’t stay confused for long. Since this is an internet-based test, YOUR ANSWERS, of course, WILL BE COMPLETELY ANONYMOUS. Nothing will be recorded by NSA , Equifax, or the Russians.

“Single-payer” means:

- socialized medicine

- 100% of health care costs are paid for with taxes

- Pop-Pop picks up the dinner bill for everyone

- none of the above

Answer: 4. none of the above – In socialized medicine health care facilities and providers are owned by the government. “Socialized medicine” is a pejorative term which is now irrelevant since at least 70% of U.S. healthcare costs are already met by tax dollars from Medicare, Medicaid, or the Veterans Administration. “Single-payer” is just an insurance scheme for public or privately owned services. In countries with universal health care insurance 77%-87% of costs are met by taxes. In the U.K. private insurance pays for about 13%. Pop-Pop gladly picks up the dinner bill for his children, but health insurance is still on them.

The number of countries with universal health insurance are:

- 1

- 2

- 3

- 58

Answer: 4. 58 – Germany in 1883, France in 1945, UK in 1946, Australia in 1975, Canada in 1984, Israel in 1995.

A basic tenet of single-payer insurance is that everyone will be covered without regard to income level:

- true

- false

- true, but …

Answer: 3. True, but … it will take years to bring everyone in the U.S. under “Medicare For All”. Each year or so another decade of ages will be added to the coverage. States will need to coordinate their income-based Medicaid programs with “Medicare For All”. Some states could request and receive waivers from the national program. Etc., etc., as incrementally we always go.

Universal health care insurance in other countries is administered:

- nationally

- regionally

- locally (municipalities)

- all of the above

Answer: 4. all of the above – Germany has 1100 public and private “sickness funds” with a national standard level of coverage. In the Netherlands health insurance is administered by municipalities that levy local taxes to pay the costs. This apparently enhances transparency and both taxpayer and patient satisfaction. Conclusion: If you have seen one system of universal health coverage, you have seen ONE. By the way, isn’t “sickness fund” a much more honest name for insurance which pays for medical care and does not necessarily buy “health”. (Leave it to the Germans to say it like it is).

Universal health insurance is based on which basic insurance principles:

- spread the risk over the greatest number of people

- use education and regulation (i.e.. fire laws) to reduce the highest risks of loss

- if you win (stay healthy), you “lose” (your premiums). If you “lose” (get sick), you win (care is paid for)

- use excess premium revenue to build fancy office buildings and pay for expensive lobbyists .

Answer: 1-3 (see subsequent question for further information on #4)

Single payer health insurance will cost less to administer than our present system:

- true

- false

- true, but …

Answer: 3. true, but… maybe not as much reduction as we hope. Administrative costs for the individual provider will probably remain the same because “meaningful criteria” compliance, complex diagnostic coding, need for medical necessity justification, and need for data showing that quality is not being eroded will continue to require significant personnel time and computer capability. Remember also that Medicare is currently administered in large part by “fiscal intermediaries” like Blue Cross. That probably won’t change. Some predict that because of continued pressure on a single-payer to reduce costs, it may, if fact, get even more complicated for providers to get paid for their services. Of course, the huge consumer advertising, employer marketing, and lobbying expenses of private health insurance companies will be greatly reduced when the market share of private insurance is reduced to 10-15% as has occurred in other countries. If only we could get Visa to run Medicare’s fraud protection system!

Why not “Medicaid For All”; could individual states institute universal health insurance so that we wouldn’t have to wait for a national consensus?

- no

- yes

- yes, but…

Answer: 3. Yes, but … the hallmark of universal health insurance in other countries is a consistent standard of coverage for all residents. Medicaid programs are state-specific and coverage is extremely variable, as is provider payments. If you see one, you have seen one. Attempts to waive the Obamacare national standards by those wishing to repeal it spotlighted the potential glaring inequities. But, Massachusetts has done it for 90% of its population, and there are bills in its legislature to do it for all. California is attempting to do it. Most California families and businesses, a University of Massachusetts study has said, would pay less for health care than they do now, even with the new taxes, because they would no longer pay premiums, deductibles or co-pays. As Samantha Bee recently noted: “You don’t have to be racist anymore to believe in States’ Rights .”

Why is a single-payer sometimes described as a “double-edged sword”?

- a single-payer could have much greater negotiating leverage with both suppliers (drug companies) and providers (doctors and hospitals)

- a single-payer would be perched on the sharpest edge of the cost-quality equation

- the standardization of payments by a single-payer could dampen innovation and hamper medical progress

- all of the above

Answer: 4. all of the above – More leverage against the drug companies is “good”. More leverage against the providers could be “bad”. Despite studies that show that good quality care is less costly, many still see a dichotomy between cost and quality. Concern about hampering innovation (“new ways of doing things”) with excessive standardization (“the old ways”) was one reason Obamacare created a Center for Innovation within Medicare as part of the ACA .

Who is in favor of single-payer health insurance?

- 60% of those polled

- 38% of those polled

- depends on the nature of the poll

- all of the above

Answer: 4. all of the above – The 60% in favor of single-payer health insurance dropped to 38% when the question was tied to one about increased taxes. The most recent Harris-Harvard poll (9/17/17) showed that 52% were in favor of single-payer insurance. 69% believe that it would provide more coverage, including 54% of Republicans. . Most of the other questions about a governmental single-payer were 50/50 pro and con. Some physicians, hospitals, and other providers are in favor of single-payer insurance.

What are some of the barriers to implementing single-payer, universal health insurance in the U.S.?:

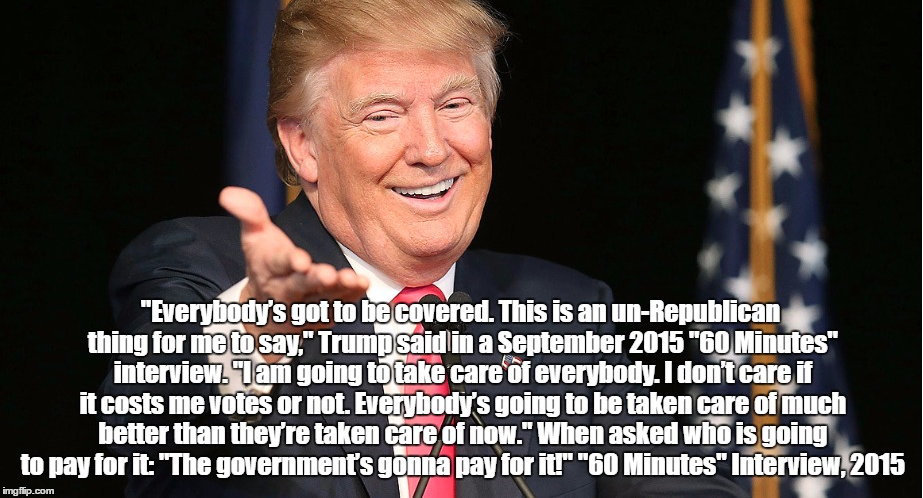

What does President Trump think?:

Posted by hubslist

Posted by hubslist